New Listings and Pending Sales

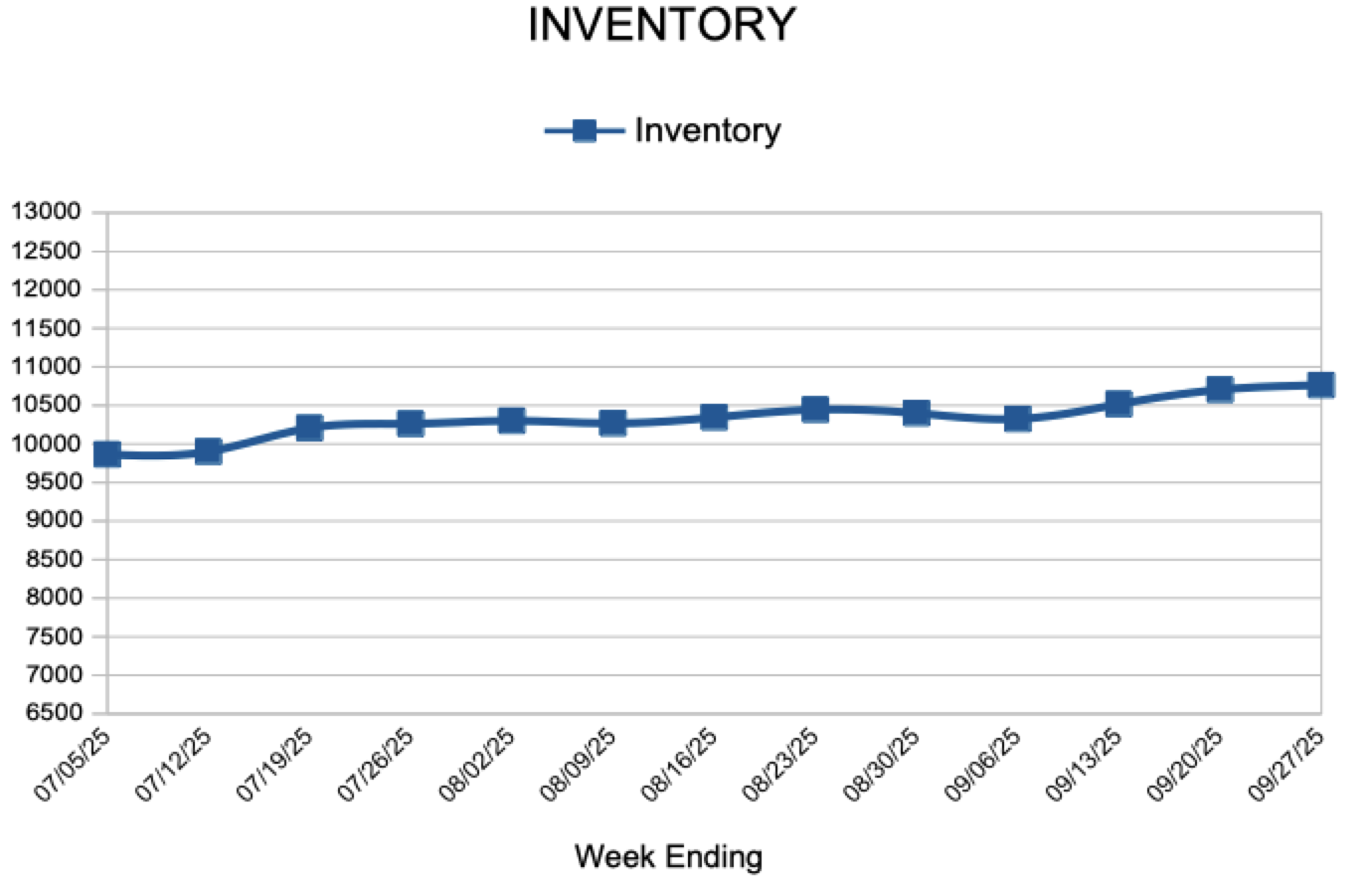

For Week Ending September 27, 2025

For Week Ending September 27, 2025

According to ATTOM’s Q2 2025 Home Equity and Underwater Report, 47.4% of mortgaged residential properties in the U.S. were considered equity-rich—defined as having at least 50% equity—in the second quarter of 2025. This marks an improvement from the first quarter, when 46.2% of mortgaged homes met that threshold, ending a trend of three consecutive quarterly declines.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING SEPTEMBER 27:

FOR THE MONTH OF AUGUST:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

October 2, 2025

The 30-year fixed-rate mortgage increased again this week but remains below its 52-week average of 6.71%. The last few months have brought lower rates and as indicated by the recently reported increase in pending home sales, homebuyers are feeling more confident to get into the market.

Information provided by Freddie Mac.

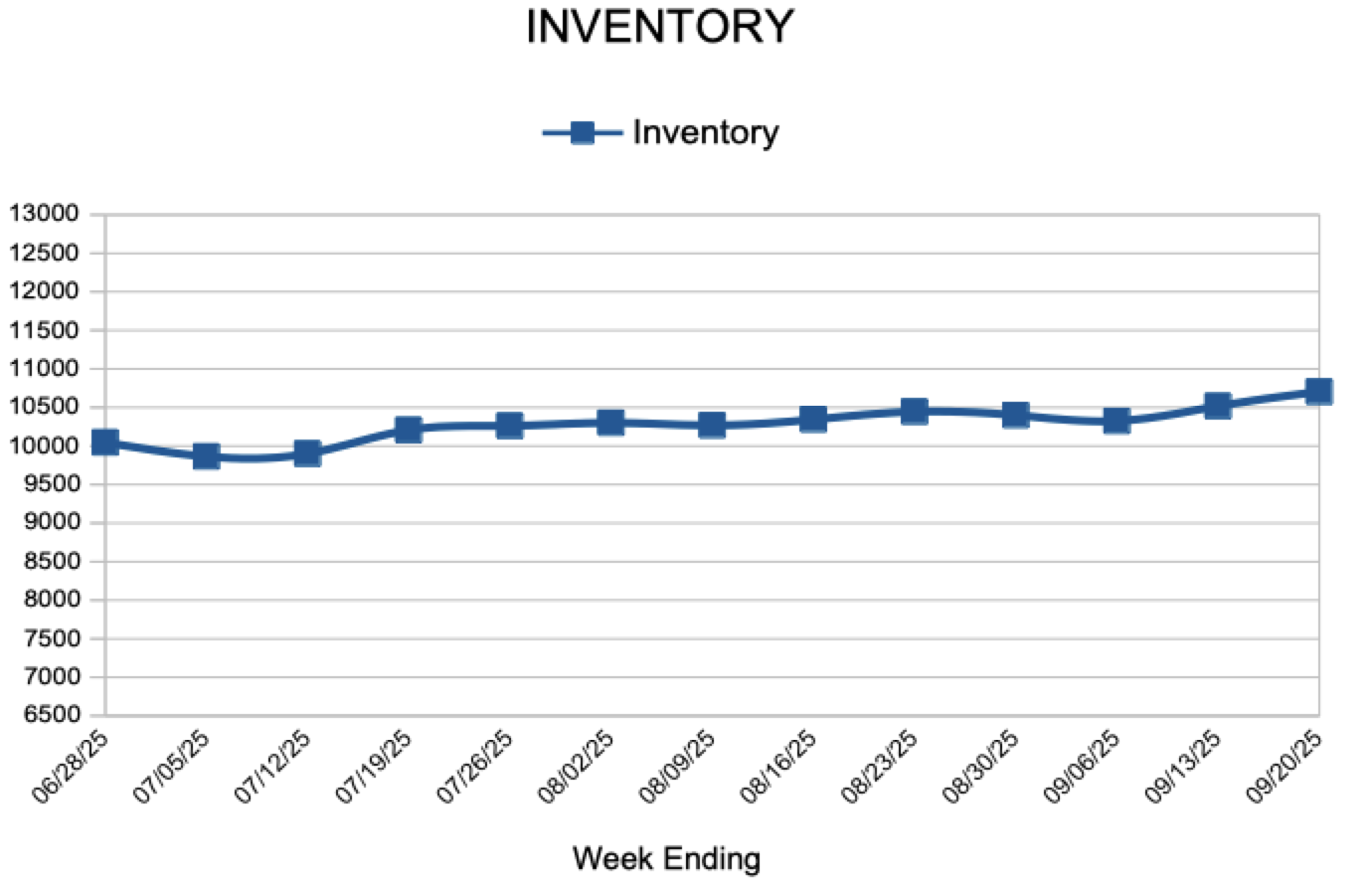

For Week Ending September 20, 2025

For Week Ending September 20, 2025

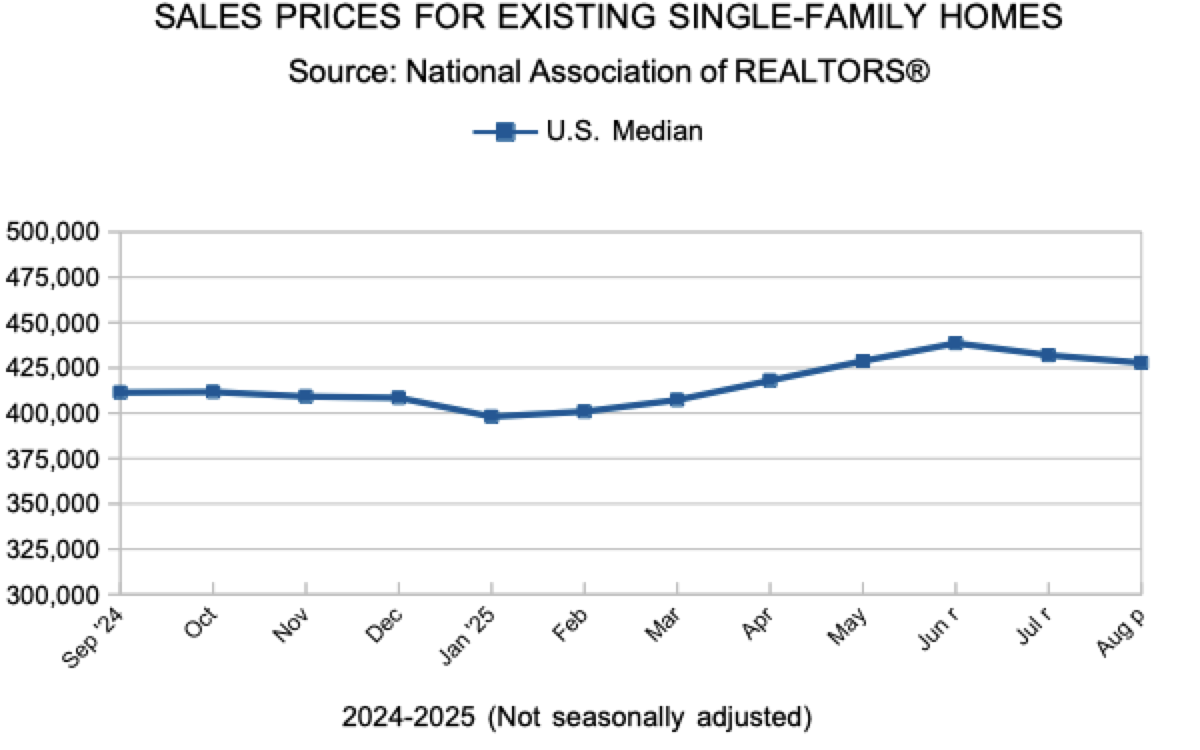

The number of homes actively for sale increased for the 22nd consecutive month, rising 20.9% year-over-year in August, according to Realtor®.com’s August 2025 Monthly Housing Market Trends Report. At the same time, the national median list price declined 2.2% from the previous month to $429,990, with 20.3% of listings receiving price cuts as sellers responded to changing market conditions.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING SEPTEMBER 20:

FOR THE MONTH OF AUGUST:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

September 25, 2025

Following several weeks of decline, mortgage rates inched up this week. Housing market activity continues to hold up with purchase and refinance applications increasing by 18% and 42%, respectively, compared to the same time last year.

Information provided by Freddie Mac.

Licensed In Minnesota

All information deemed reliable but not guaranteed and should be independently verified.