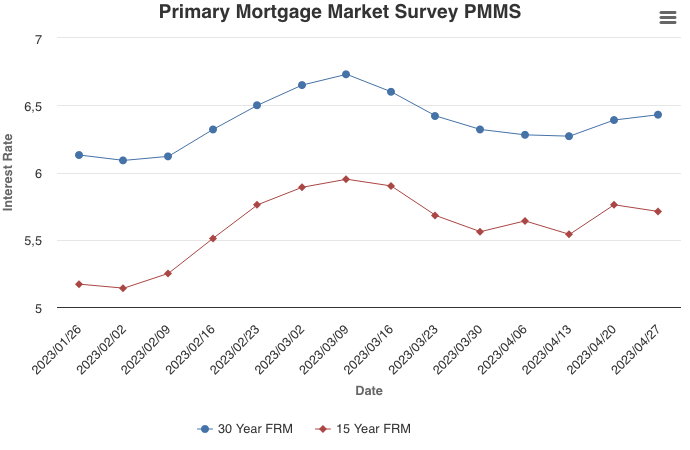

April 27, 2023

The 30-year fixed-rate mortgage increased modestly for the second straight week, but with the rate of inflation decelerating rates should gently decline over the course of 2023. Incoming data suggest the housing market has stabilized from a sales and house price perspective. The prospect of lower mortgage rates for the remainder of the year should be welcome news to borrowers who are looking to purchase a home.

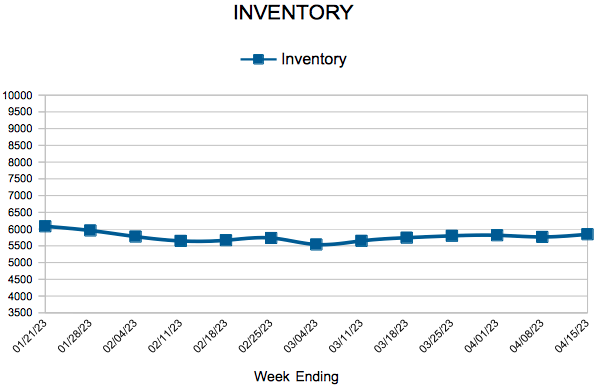

Information provided by Freddie Mac.

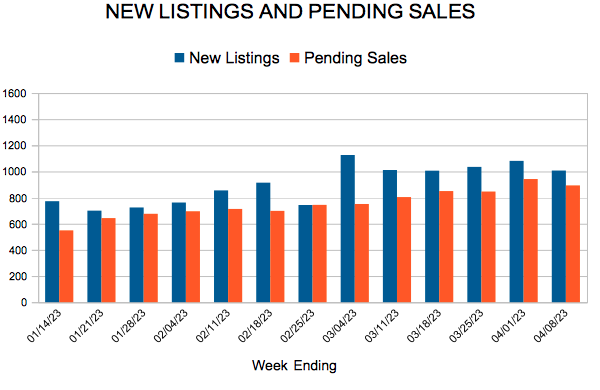

For Week Ending April 15, 2023

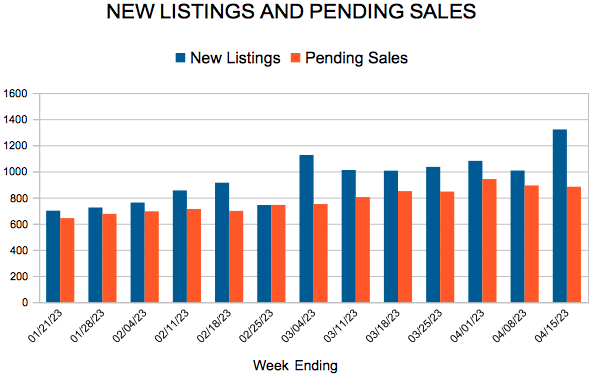

For Week Ending April 15, 2023