For Week Ending May 2, 2026

A family earning the U.S. median income of $104,200 needed to spend 34% of its income on the mortgage for a median-priced new home ($405,300) in the fourth quarter of 2025, down from 35% in the third quarter, according to the National Association of Home Builders/Wells Fargo Cost of Housing Index.

In the Twin Cities region, for the week ending May 2:

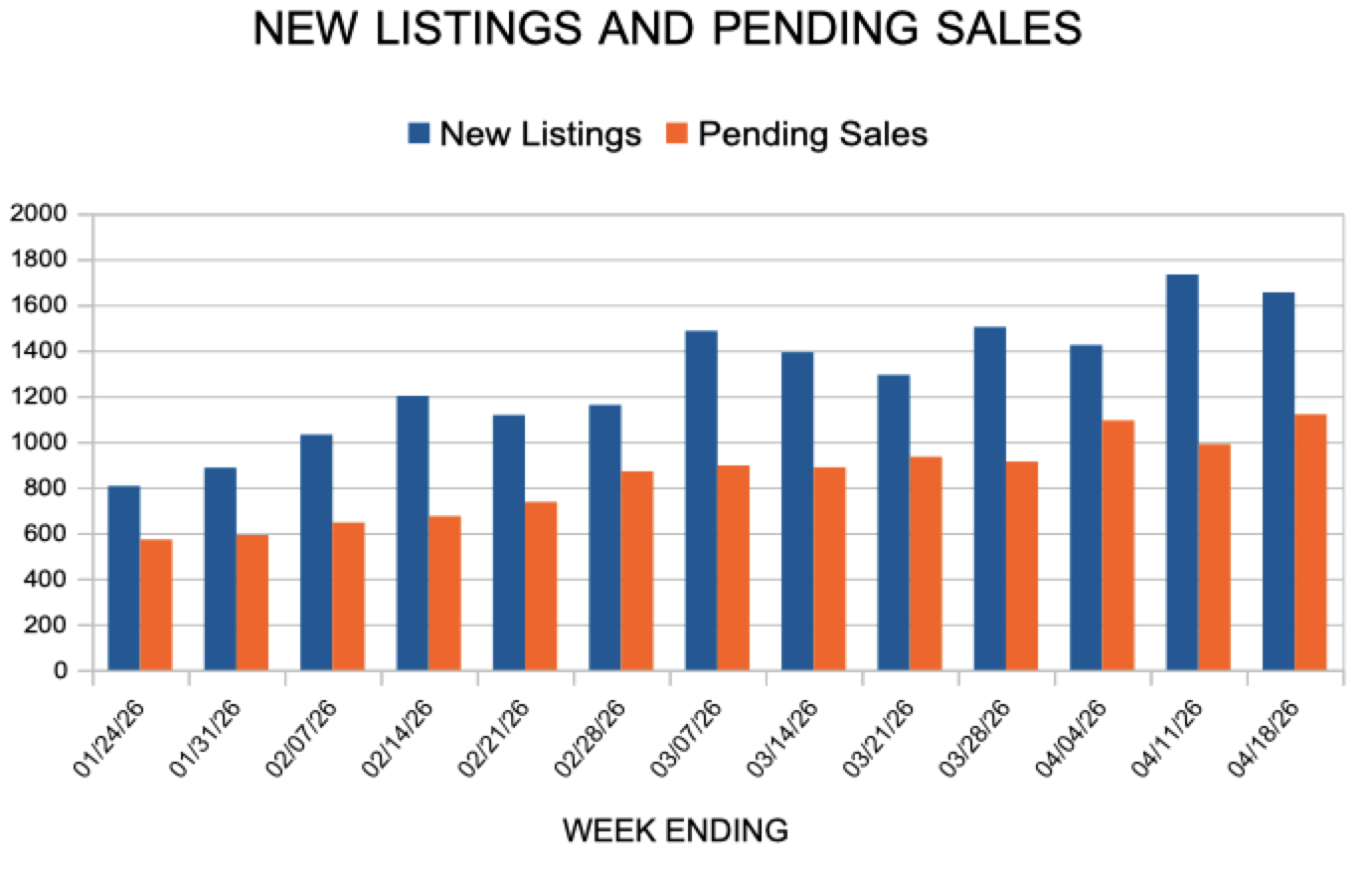

- New Listings increased 10.4% to 1,855

- Pending Sales increased 3.5% to 1,197

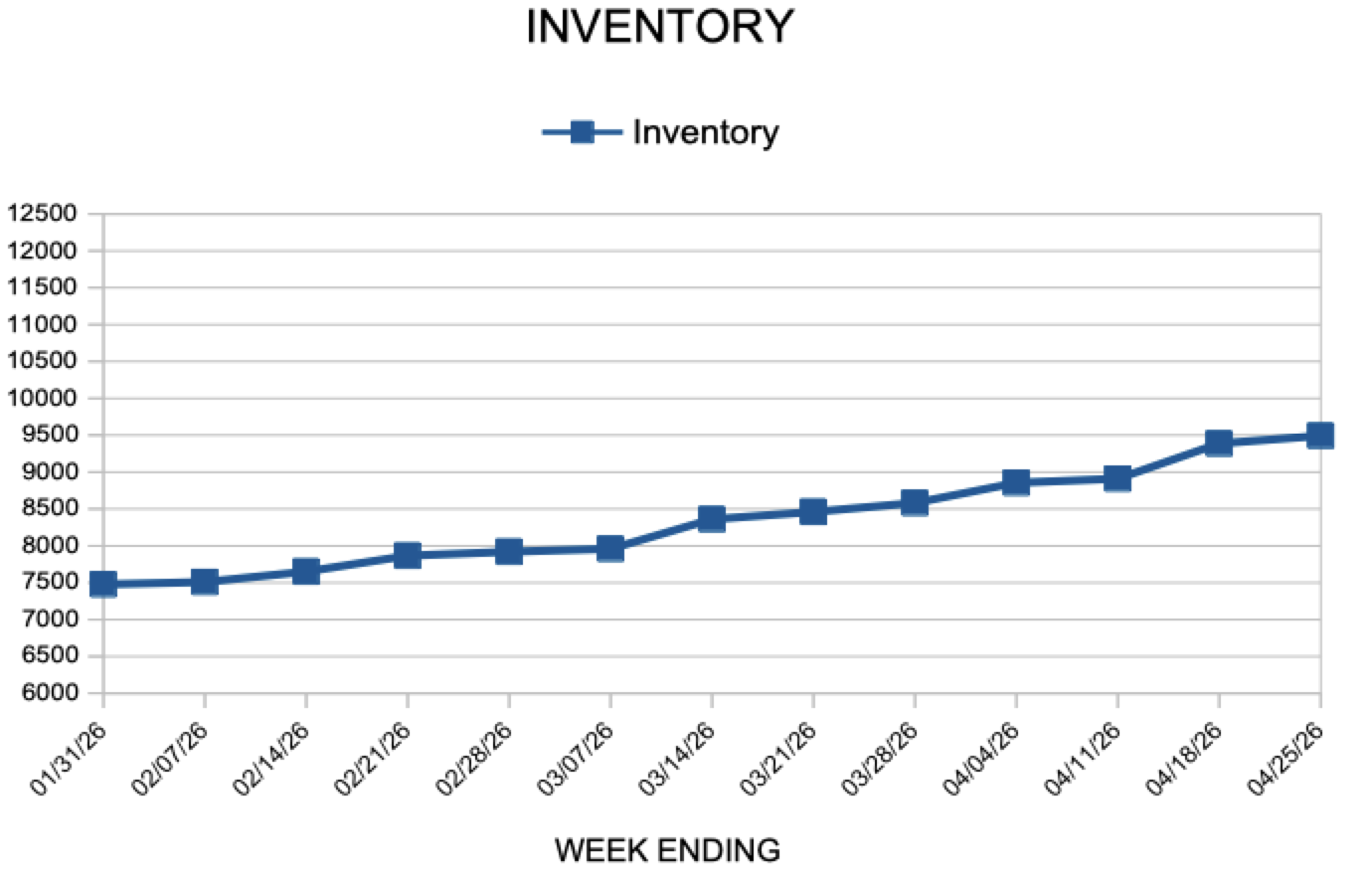

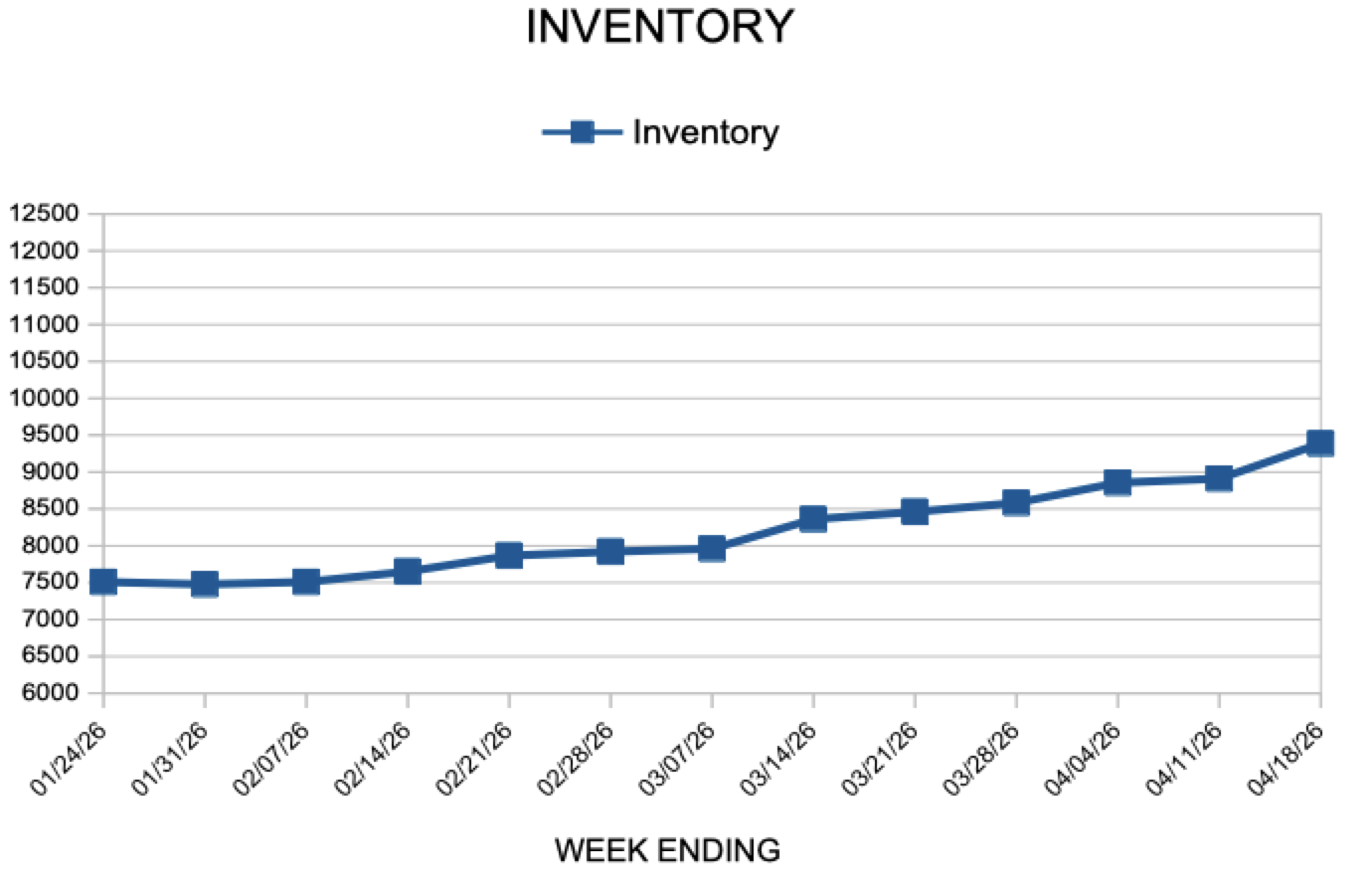

- Inventory increased 8.1% to 9,815

For the month of March:

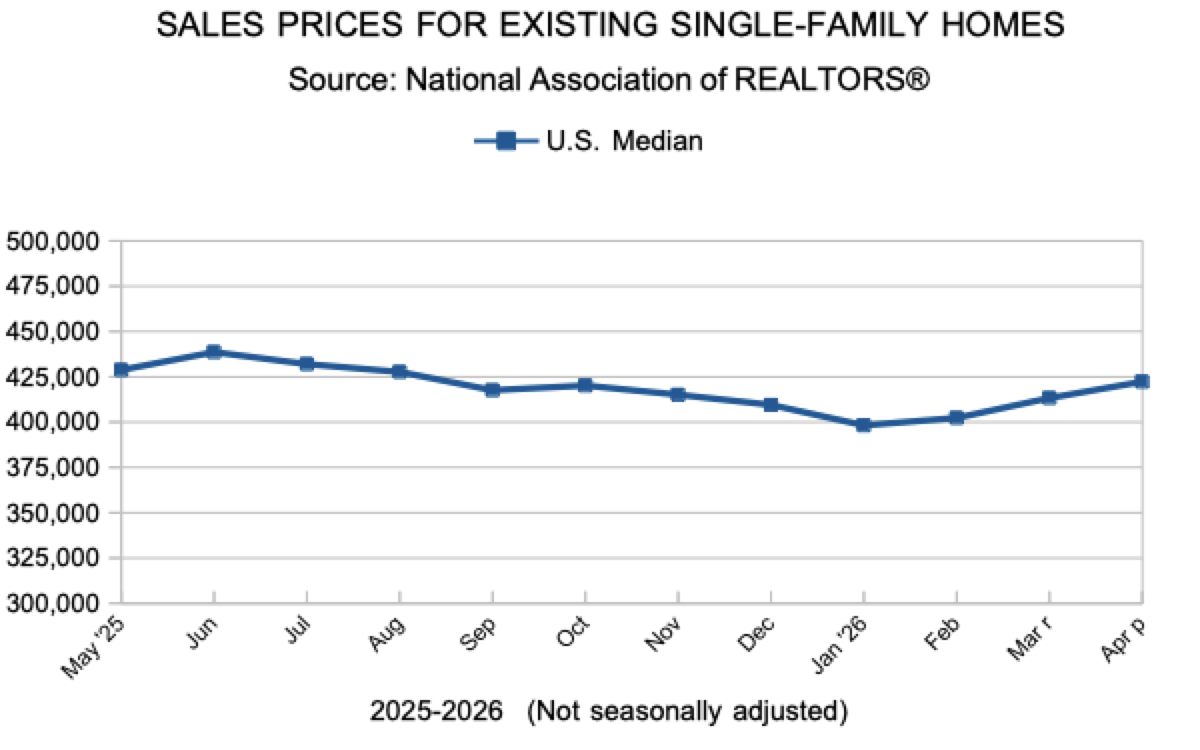

- Median Sales Price remained flat at $380,000

- Days on Market increased 6.8% to 63

- Percent of Original List Price Received decreased 0.5% to 98.5%

- Months Supply of Homes For Sale increased 9.1% to 2.4

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.