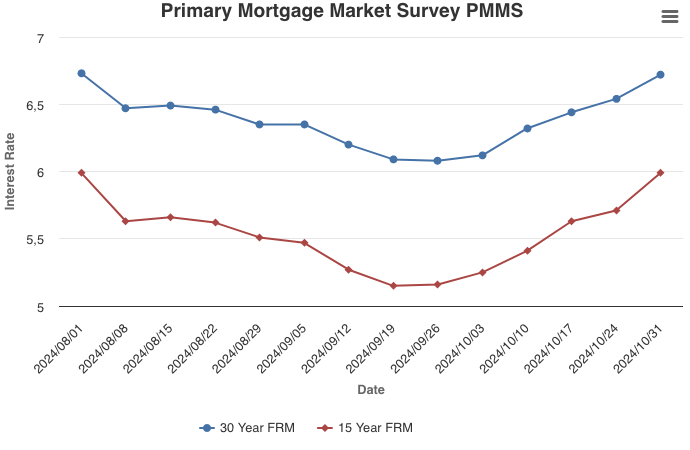

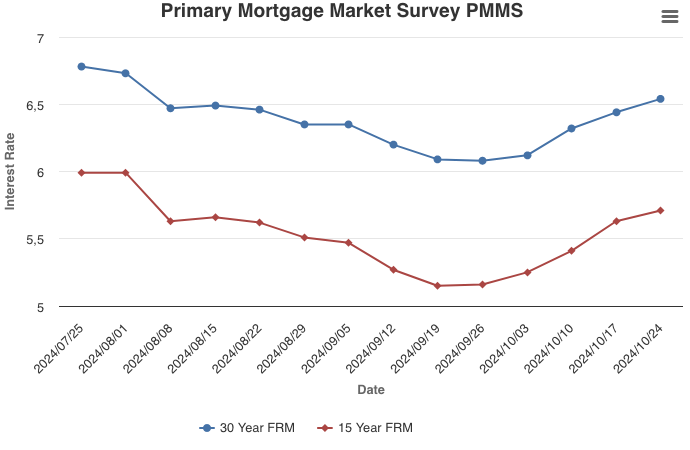

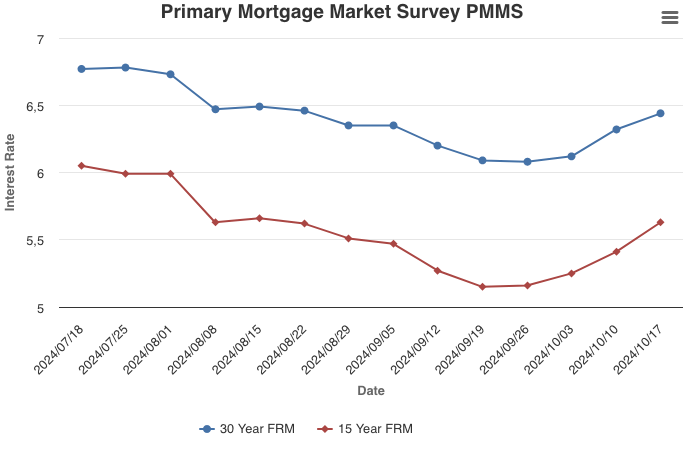

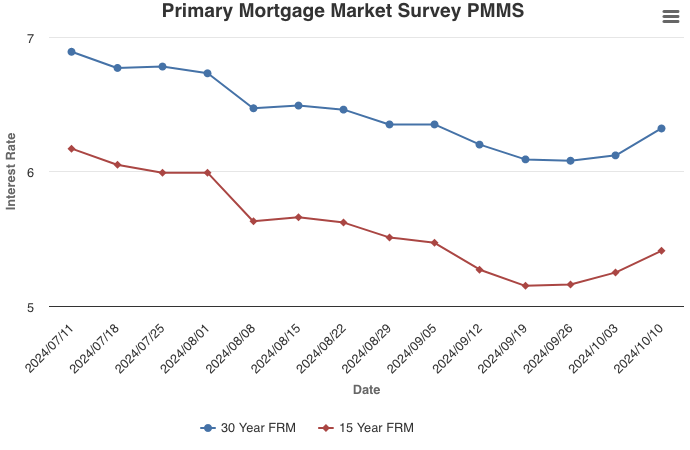

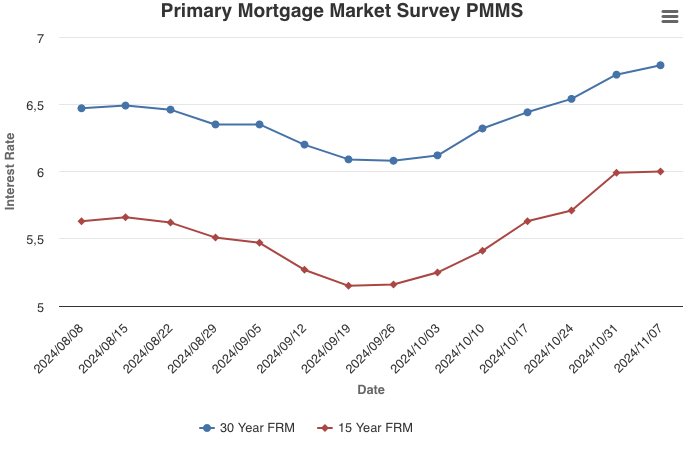

November 7, 2024

Mortgage rates continued to inch up this week, reaching 6.79 percent. It is clear purchase demand is very sensitive to mortgage rates in the current market environment. As soon as rates began to rise in early October, purchase applications fell and over the last month have declined 10 percent.

Information provided by Freddie Mac.