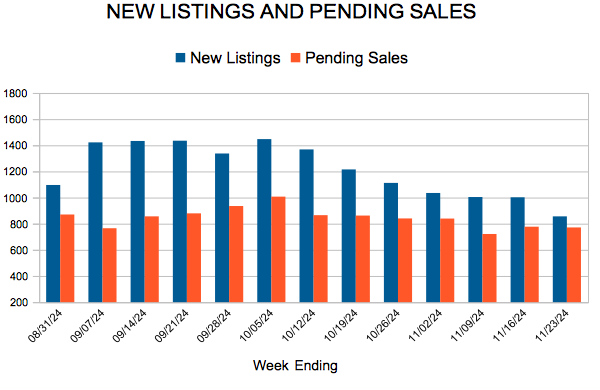

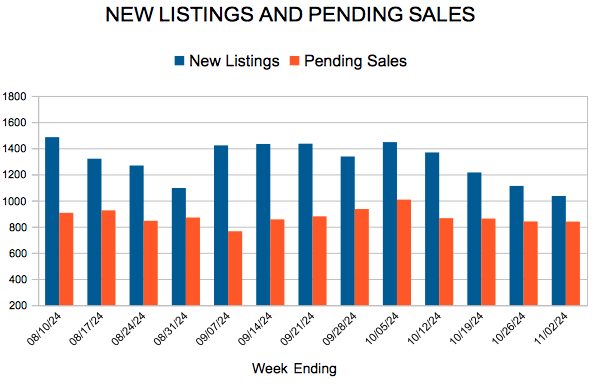

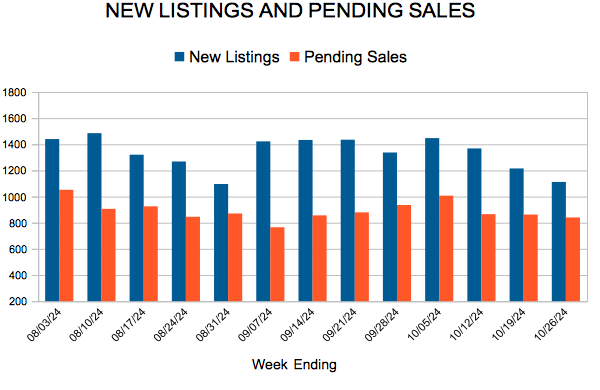

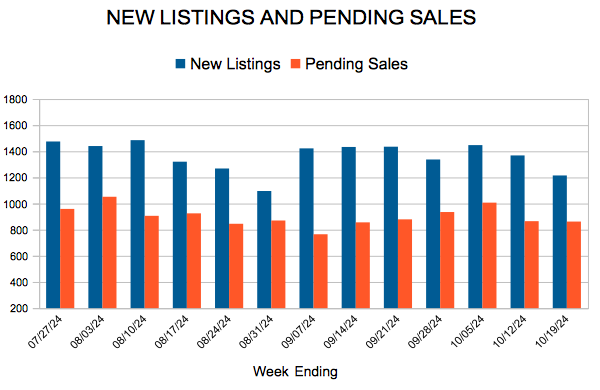

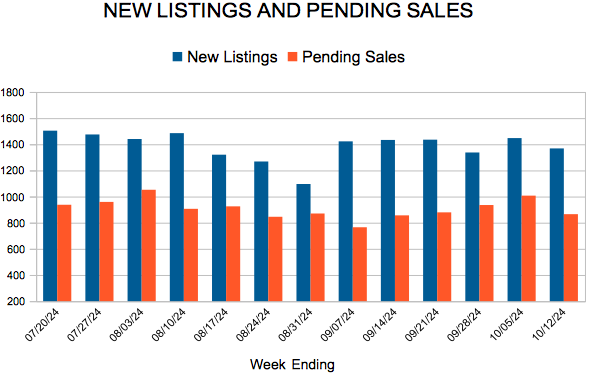

New Listings and Pending Sales

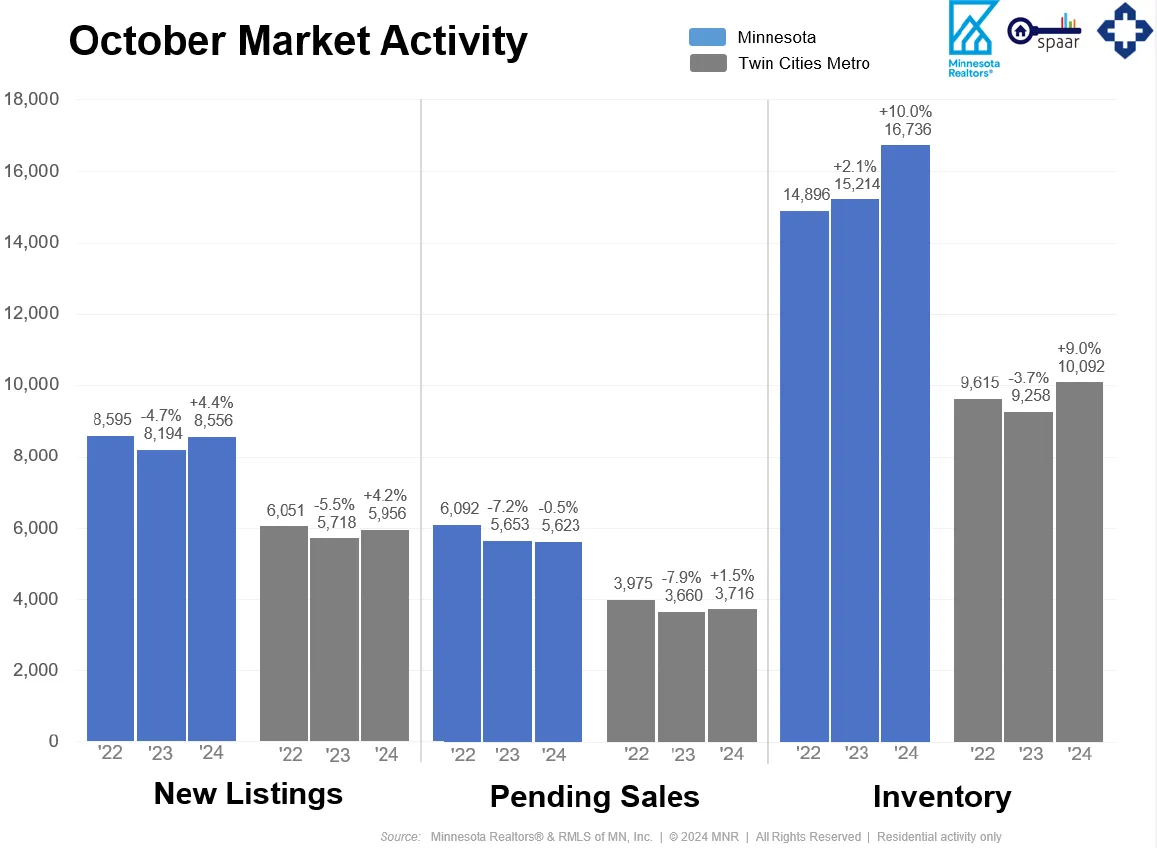

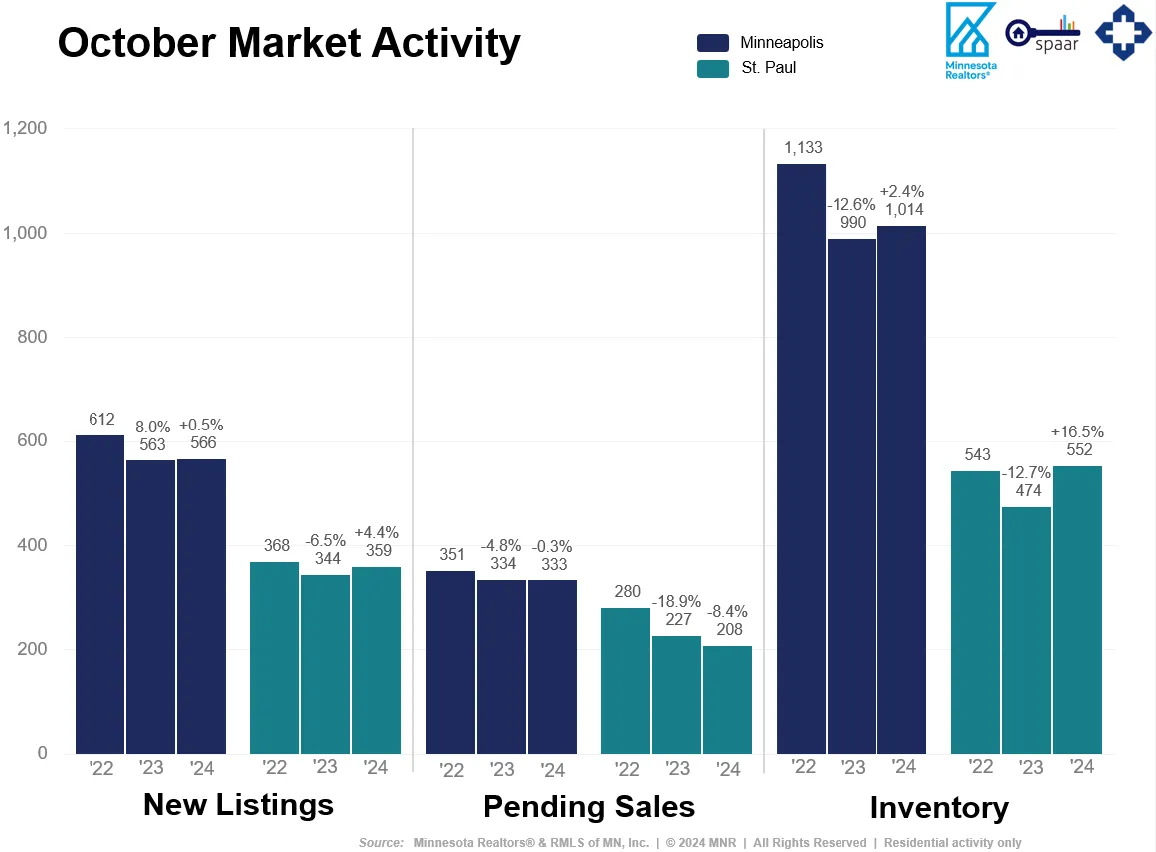

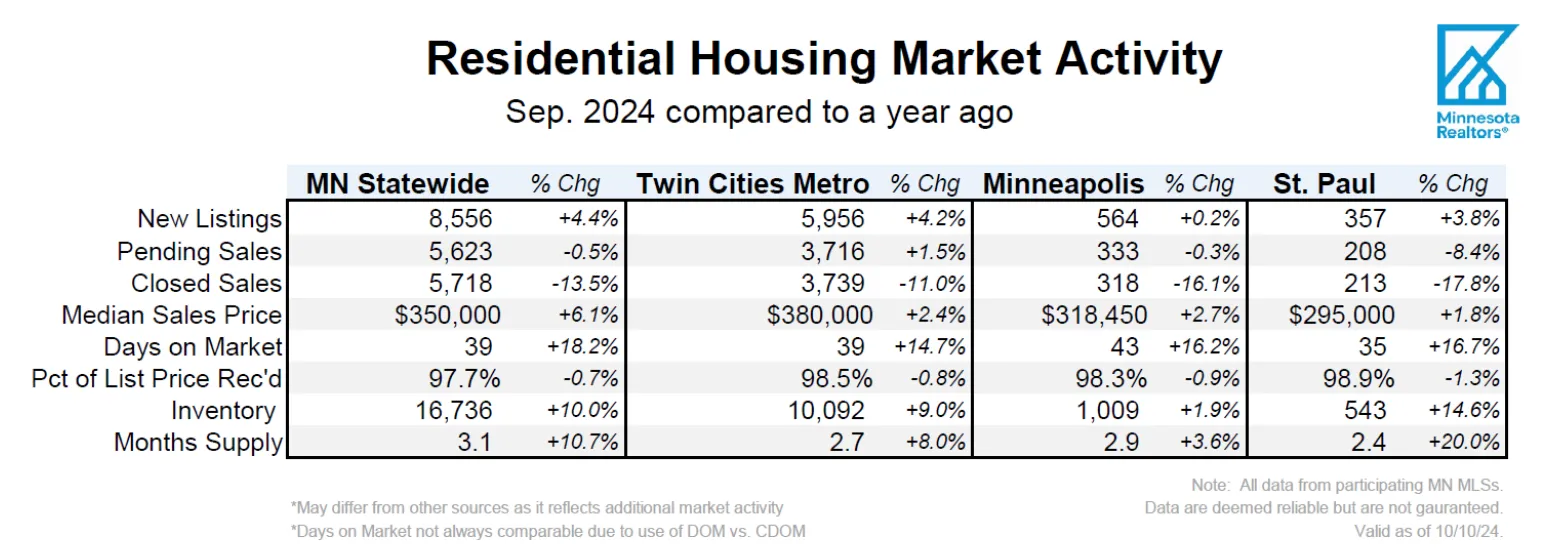

(Nov. 14, 2024) – According to new data from the Minnesota state and Twin Cities metro REALTOR® Associations, listings, sales, prices and inventory all rose in October.

Sellers, Buyers and Housing Supply

Mortgage rates hovered between 6.0–7.0% all month long, but buyers seem to be adjusting to the current rate environment as pending sales rose a strong 10.4% statewide and 14.3% in the metro. The average 30-year mortgage rate was 6.18% in September and 6.43% in October. With the exception of September, rates haven’t been that low since May of 2023. The pent-up activity is on the supply side, too. Most sellers are also buyers, and those who chose to delay their move are getting restless. While they’ll be met with more inventory, they may not see the most ideal interest rate. Still, new listings were up 9.1% statewide and 8.7% in the metro compared to last October.

Despite recent gains, supply levels remain low due to a lack of new home construction. Existing sellers who would ordinarily move up the housing ladder and free up their first-time home feel “locked in” to their favorable mortgage rates. Those rates are often between 3.0–4.0% or lower compared to nearly 7.0% today. The Federal Housing Finance Agency (FHFA) has found that about 70% of all outstanding mortgages are financed below 4.0%. There are signs of change, but housing demand has fallen due to the affordability crisis. The persistent housing shortage kept home prices rising, just as the Federal Reserve hiked interest rates to combat inflation. Prospective home buyers are still feeling the triple punch of higher prices, higher mortgage rates, and limited inventory. While home prices are still rising, wage growth has been exceeding the rate of inflation. In fact, the U.S. Bureau of Labor Statistics reports that wages are rising at 4.6% while inflation is rising at 2.4%.

“We see buyers adjusting to today’s mortgage rates, but experienced Realtors know there are many ways to get deals done,” said Geri Theis, President of Minnesota Realtors®. “Having a strong Realtor negotiating on your behalf, directing you to down payment resources and offering suggestions on timelines and contingencies will help you stand out against your competition and ultimately help you close the deal.”

Prices, Market Times and Negotiations

Every area and market segment is unique. Some listings are getting multiple offers and closing for over list price. But overall, sellers accepted offers at 97.1% of list price statewide and 97.8% in the metro—both down from last year. And those offers were accepted after an average of 42 days on market statewide and 45 days in the metro—both figures up from a year ago. “We’re seeing different activity in different price points, areas and segments such as condos or new construction,” said Jamar Hardy, President of Minneapolis Area REALTORS®. “What’s impacting $1M+ buyers isn’t necessarily on the mind of a $300,000 buyer, and condos and new construction are better supplied and more accessible than the existing single-family market, for example.”

The state median home price was up 5.3% to $347,500, and the metro median price was up 4.1% to $380,000. A slowdown in price growth would give incomes a chance to catch up, helping address affordability concerns. And additional inventory will mean less upward price pressure from a persistent supply shortage. It would also allow buyers to have more options from which to choose. “Sales numbers confirm some of the renewed optimism I’m seeing in today’s housing market given better rates and more inventory,” said Amy Peterson, President of the Saint Paul Area Association of REALTORS®. “While many sellers and buyers feel now is the right time to make a move, it’s still important to consider their goals in taking that next step and negotiating offers.”

Locational Differences | Minnesota statewide

Market activity always varies by area, price point and property type. Regions such as Duluth and the North Shore and Hibbing/Virginia saw the largest gains in seller activity. Alexandria, St. Cloud and the Twin Cities had the largest gains in pending sales. Homes sold the fastest in the Duluth/North Shore region along with St. Cloud. Prices were highest in the metro followed by Detroit Lakes and Rochester. The most affordable regions of the state were Hibbing/Virginia and Willmar. Every region is undersupplied except Hibbing/Virginia, Detroit Lakes and Bemidji, which are relatively well balanced.

Locational Differences | Twin Cities Metro

For cities with at least five sales, Afton, Columbus and Arden Hills had the largest sales gains. The highest priced areas were Orono, Afton and North Oaks while the most affordable areas were South St. Paul, Brooklyn Center and Isanti. But the largest increases in sales price were in Afton, Orono and Hopkins. The most oversupplied markets were Clear Lake, Centerville and Cokato while the most undersupplied markets were Oak Park Heights, North St. Paul and Mound. Homes took the longest to sell in Mayer, Columbus and Centerville and sold the fastest in Norwood, Greenfield and New Brighton.

From The Skinny Blog.

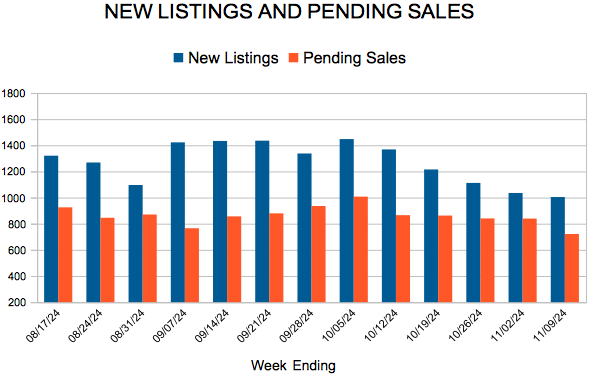

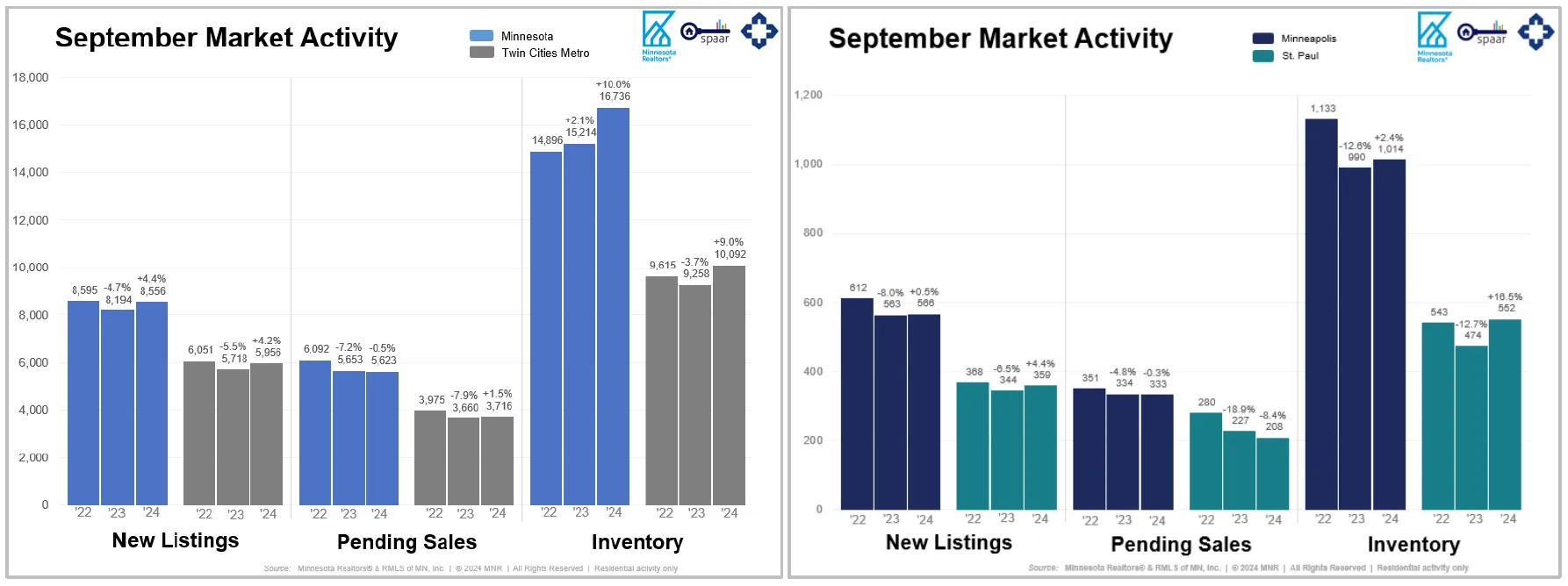

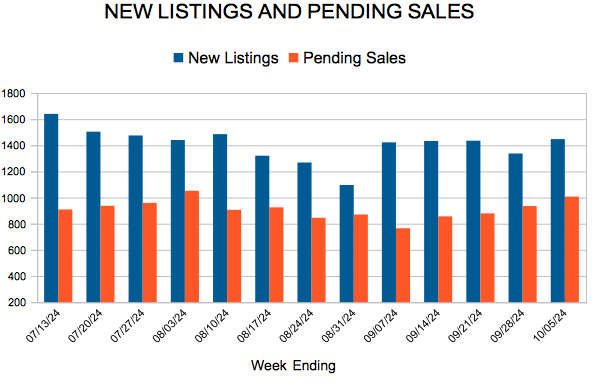

(Oct. 15, 2024) – According to new data from the Minnesota state and Twin Cities metro REALTOR® Associations, listings rose compared to last year while sales were flat. Inventory and prices are both up.

Sellers, Buyers and Housing Supply

It’s no secret that buyers have been facing a triple punch lately: higher prices, higher mortgage rates and tight inventory. That’s shown up in slower sales activity, lower affordability and slim pickings when it comes to the number of homes for sale on the market. In fact, statewide, sales hit their lowest level since 2011, but now signed purchase agreements are rising. Sellers are caught in between—either they stay put in a home they might have outgrown or trade up to a higher price, higher mortgage rate and higher monthly payment. But there’s evidence that’s changing.

For example, the state and metro saw 4.4% and 4.2% more new listings, respectively, when compared to September 2023. For sales, statewide activity was relatively flat (down 0.5%) while metro-area activity rose a modest 1.5%. The fact that listing activity has been stronger than sales means inventory levels are up—most recently rising an even 10%. But we’re still in a sellers’ market. Lower inflation, stronger-than-expected hiring and the Federal Reserve’s mid-September rate cut are all reassuring signs for home buyers. That’s not to say there are no concerns about housing or the economy. For now, however, this marginally better confidence is helping to stabilize home sales and slightly improve affordability.

When it comes to mortgage rates, be careful what you wish for. Rates back below 5% could mean recession. The fact that so many homeowners enjoy rates below 4% creates the “lock-in effect” where would-be sellers choose to stay put instead of trading up to a higher price and higher rate. “There is still plenty of pent-up activity both buyers and sellers—who are being patient,” according to Geri Theis, President of Minnesota Realtors®. “That sounds like a good idea until you realize everyone else is waiting for the same thing. And as rates come down, some may find themselves in another competitive environment where listings are selling for over asking price,” she added.

Prices, Market Times and Negotiations

All situations and transactions are unique. First-time buyers without equity have an uphill battle while move-up buyers with equity from their first home are able to roll that into the next property. The more affordable price points have seen the largest declines in demand as those buyers are more rate sensitive. Luxury market activity continues to outperform as those buyers are less rate sensitive. Sales at or above $1M have risen 16.8% over the last 12 months, more than any other price point. Those relocating here with equity from higher-priced coastal markets should face fewer headwinds. And each market segment is unique as well. Some listings are still getting multiple offers and selling for over list price. Overall, however, sellers accepted offers at 97.7% of list price statewide and 98.5% in the metro. Both figures were down from last year. And those offers came in after an average of 39 days on market both statewide and in the metro—both figures up from a year ago. “There are significant differences from price point to price point and area to area,” said Jamar Hardy, President of Minneapolis Area REALTORS®. “Buyers were excited as rates hit the low sixes even though they’ve trickled higher since, and I believe we’ll see a real boost if and when we go below 6%.”

The state’s median home price was up 6.1% to $350,000; the metro median price was up 2.4% to $380,000. Since 2021, the typical mortgage payment on the median-priced Twin Cities home has risen from around $1,750 to $2,750 per month. Most economists agree that the path for rates should be lower, but it will be bumpy on the way down. What’s also true is that incomes are and have been rising faster than home prices. That should give households a chance for earnings to catch up to home prices. In the meantime, more supply will mean less competition and more choices, which should translate into better affordability and more manageable price growth. “I have buyers who are pleased to see more options to choose from,” said Amy Peterson, President of the Saint Paul Area Association of REALTORS®. “But for the most part sellers still hold the reigns even with the extra inventory we’ve seen.”

Location Differences | Minnesota Statewide

Market activity always varies by area, price point and property type. Regions such as Hibbing/Virginia and Bemidji saw the largest gains in new listings. Bemidji also saw the largest gain in pending sales and now has 6.2 months of supply—the most of any region. St. Cloud and Grand Rapids also had notable increases in sales. Homes sold the fastest in the Duluth/North Shore region along with St. Cloud and the core Twin Cities. Prices were highest in the metro followed by Detroit Lakes, Alexandria and Brainerd. The most affordable regions of the state are Hibbing/Virginia, Bemidji and Willmar.

Location Differences | Twin Cities Metro

For cities with at least five sales, Deephaven, Maple Plain and Mayer had the largest sales gains. The highest priced areas were Deephaven, Wayzata, Orono and Medina while the most affordable areas were Hutchinson, Norwood Young America and Robbinsdale. But the areas with the largest increases in sales price were Deephaven, Orono and Little Canada. The most oversupplied markets were Centerville, Hanover and Wayzata while the most undersupplied markets were Circle Pines, Crystal and New Hope. Homes took the longest to sell in Bayport, Annandale and Orono and sold the fastest in Corcoran, Arden Hills and Circle Pines.

From The Skinny Blog.

Licensed In Minnesota

All information deemed reliable but not guaranteed and should be independently verified.